Will 2018 be appealing to global polyester markets?

2018 is expected to shape up in an interesting year for global fibre markets. In cotton, there will be an additional 3 million ton (17.6 million bales of 170kg) of production. At the same time, world’s polyester staple fibre market will have to adjust to China’s ban on import of solid waste from January 2018. This ban includes an estimated 2.5 million ton of PET waste that is used to produce recycled polyester including staple fibre and filament. The ban has already pushed prices up of both recycled and virgin staple.

Things have started to change with the banning the import of solid waste which includes raw materials for recycled PSF. In the short run, alternative global sources of rPSF cannot replace falling Chinese exports and China may even seek to import rPSF to supplement its own reduced activity.

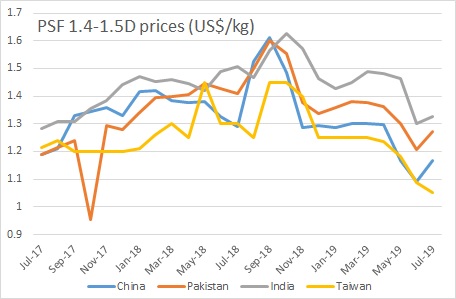

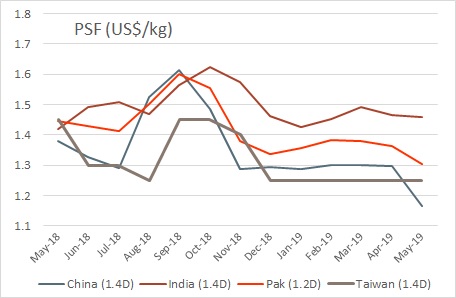

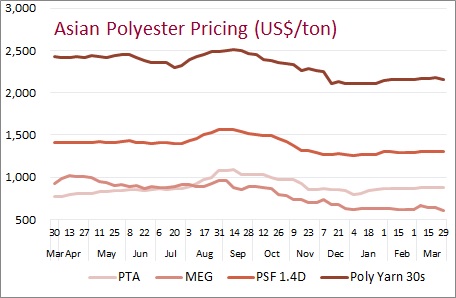

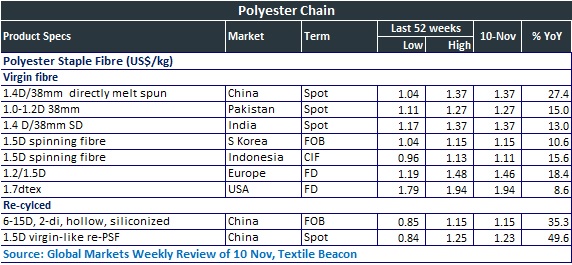

In the week ending 10 November, virgin PSF prices have jumped 10-28% year on year in most Asian markets. Since the announcement of up-coming ban on waste in China, recycled markets have started looking for alternatives to replace this huge void that would be created from 1 January. Meanwhile, r-PSF prices have surged 35-50% in China’s domestic markets. And the gap between the two, virgin and recycled PSF has narrowed down to US cents 15 a kg from the widest US cents 20 a kg during the last 52 weeks.

In the week ending 10 November, virgin PSF prices have jumped 10-28% year on year in most Asian markets. Since the announcement of up-coming ban on waste in China, recycled markets have started looking for alternatives to replace this huge void that would be created from 1 January. Meanwhile, r-PSF prices have surged 35-50% in China’s domestic markets. And the gap between the two, virgin and recycled PSF has narrowed down to US cents 15 a kg from the widest US cents 20 a kg during the last 52 weeks.

China, the major global supplier of polyester fibre including recycle-based PSF, produces over 4 million ton of rPSF which is used in domestic spinning and nonwovens and is also exported in fibre form. China has huge overcapacity in rPSF, with around 50% capacity utilization. There is thus a perception that rPET is a cheap alternative to virgin polymer both for commodity use and in branded sales which value a claim of recycled content.

As China cleans up its act a new global PSF supply chain will emerge. The raw material supply chain of recycle-based polyester staple fibre (rPSF) is being disrupted by new environmental considerations in China, and this will have a wide spread global impact.

Outside China, there is no capacity to replace Chinese rPSF supply. So, while raw material (flake) prices should fall in the rest of the world, rPSF prices are rising more or less in line with Chinese rPSF export offers. Higher rPSF prices can provide the commercial incentive to speed up innovation in recycling textiles and apparel, and China can emerge as the hub of clean recycling technology and raw material, that so many brands, retailers and customers claim to want and be willing to pay for.

Impact on other fibres

Short supply and higher prices for r-PSF are already supporting demand for virgin PSF, and for virgin chip as some r-PSF producers step up the level of virgin feed. Chinese producers should be able to meet the extra demand quickly as utilisation rates are not high.

But rising PSF prices could open the door for greater cotton demand. Cotton can meet additional demand through to next season without too much pressure on prices, should cotton prices remain around US cents 70-80 per pound, and China having sufficient cotton to meet additional demand. Attractive cotton prices could also mean good sowing in 2019-20 and cotton could roll back some of the polyester assault it has faced in recent years.

Viscose fibre is expensive and good quality is even more expensive, but limited in supply. VSF prices are higher and the spread against polyester has risen from US$40 a ton to US$100 a ton in the past 2-3 years. The rising PSF prices would reduce this gap in the short term which can improve the relative competitiveness of viscose. However, with huge VSF capacity expected to come up, VSF prices itself will probably come under pressure – and PSF prices may not be high enough for long to make a difference. But lower viscose prices may expose some inefficient assets and this together with tighter environmental regulations adopted in China, may result in consolidation of these capacities, cleaning up the sector.

Cotton fibre will be a favourable option to replace PSF, although the latter has been the front runner to acquire larger market share in fibre demand. The 2017-18 cotton marketing season is slated to see pricing in the band below the previous season as large cotton supplying economies are recording bumper crop this year as a surplus of 3 million ton is expected to enter the market.

SOURCE: Textile Beacon’s Global Markets Weekly Review