Polyester raw materials gearing to end 2017 on strong note

In a week before the close of 2017, polyester raw materials and feedstock markets were much ahead of their start for the year and were geared to end on a strong note. The year long journey saw feedstock – ethylene and paraxylene prices gain significantly also pulling up with them polyester intermediates – MEG and PTA prices. So, polyester chip could not be left either.

Following is the synopsis of the market trend and pricing movement of polyester chain in the week ended 22 December, one before the last week of 2017.

Ethylene market sentiment remained buoyed in Asia on healthy buying interest and beginning of the negotiations for 2018 term contract. Reportedly, suppliers pegged offers at a premium of around US$30-35 higher than a major settlement premium of US$50-55 for 2017. This has taken buyers by surprise. In Europe, activity was winding down in ethylene markets ahead of the year-end, but outages and production hiccups, pushed spot up while ethylene prices were steady-to-up in US. Asian markers, the NE CFR jumped US$30 a ton on the week while SE CFR rose US$50 a ton. While In US, spot for prompt month inched up US cents 0.50 per pound FD USG. European spot was up Euro20 on the week while CIF values were up US$37 a ton.

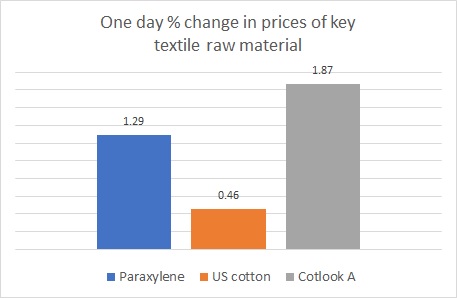

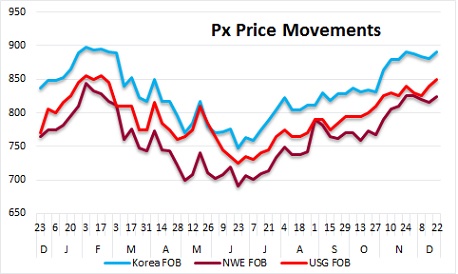

Paraxylene or Px prices moved up in Asia influenced by firming energy complex and higher January nominations over December settlement. In US, spot prices rose but the spread from mixed xylenes narrowed on proportionately rising latter prices, suggesting weak margins for producers. In Europe, Px spot inched up taking cues from Asia and tight domestic supply. The CFR Taiwan/China marker was up US$10 a ton week on week while isomer-grade MX prices also gained US$8 a ton FOB Korea. European spot also inched up US$8 a ton FOB Rotterdam while US spot  prices surged US$15 a ton seeing MX gaining US$15 a ton.

prices surged US$15 a ton seeing MX gaining US$15 a ton.

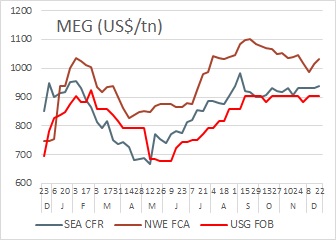

Mono ethylene glycol prices in Asia were pulled up early and then softened later but posted weekly rise of US$6 a ton CFR China. European MEG spot truck prices rose Euro 10 a ton as sentiment remained firm, despite markets ending on a quiet note ahead of Christmas break. Meanwhile, December MEG contract was agreed at an increase of Euro 20 from November. In US, MEG prices were stable as there was some demand coming from the de-icing and antifreeze sectors due to winter weather

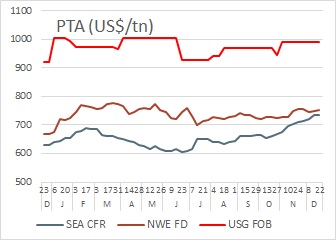

Purified terephthalic acid markets, one of the key polyester raw materials, gradually entered into a weak zone as prices remained flat initially and moderated on last two days as Christmas Day holiday drew closer. Prices  could not be swayed away by late recovery in Px cost. Demand was weak with players cautiously cutting polyester production. In US and Europe, demand for PTA was flat pegging prices stable. The CFR China marker retreated US$10 and FE & SE FOB was down US$5 a ton on the week. In India, prices edged down US$5 a ton.

could not be swayed away by late recovery in Px cost. Demand was weak with players cautiously cutting polyester production. In US and Europe, demand for PTA was flat pegging prices stable. The CFR China marker retreated US$10 and FE & SE FOB was down US$5 a ton on the week. In India, prices edged down US$5 a ton.

Polyester chip prices moved up in a narrow range amid quiet and stable market sentiment. By week end, offers edged up and values extended similar movement on the back soft PTA futures. Semi dull chip offers regained US$15 a ton while super bright chip offers rose US$10 a ton on the week.

As the polyester raw materials end strongly, 2018 will open a new chapter of competence over environment and a shake-up can be expected in the chase of producing low cost polyester materials.

Source: Global Markets Weekly Review

For complete detail report, write to us at sales@textilebeacon.com