Why did polyester prices remain flat in the last week of March

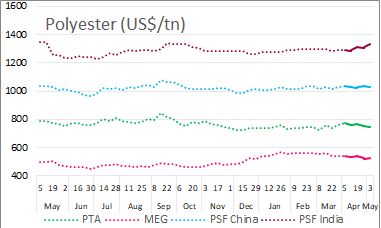

Polyester fibre (PSF) prices remained unchanged across China, India and Pakistan in the last week of March due to stable but weakening cost support. In China, PSF markets were on a weak note, dragged by softening feedstock values. In Pakistan, the market showed moderate performance and producers maintained stable operation amid ample supply. In India, PSF makers did not change their offers, as cost support was still strong amid sluggish demand. Thus, offers may go down in April.

Polyester spun yarn prices changed marginally in China, India and Pakistan as PSF prices remained frozen across markets. In China, offers for 32s and 50s spun polyester yarn rolled over while 60s yarn was cheaper implying weak demand and high inventory. In India, polyester yarn prices did not change for the third consecutive week while they remained unchanged in Pakistan for the month now.

Polyester filament yarn (PFY) prices were kept stable in China, but some producers reduced discounts as buying activity was seen improving, especially for POYs. In Pakistan, offers for both local and imported goods were raised as the currency weakened against the US$. Demand was still bearish at the moment but is expected to look up in coming weeks. In India, POYs offers were unchanged given the gentle trading atmosphere and most deals focused on multi-end specs

Upstream, purified terephthalic acid (PTA) markets firmed up late in the week in Asia as domestic prices in China gained while US$-based markers edged down a bit on fluctuating crude oil prices. The market saw April cargoes on sale while inventories were moderate with many units were under maintenance. In Europe, no development was reported from PTA market. In US, March PTA contracts were raised on higher paraxylene contracts and slightly improving downstream demand, particularly PET.

MEG prices declined in Asia on rising inventory levels and production cost pressure. Producers were under severe margin pressure due to continual price falls, which led to a shrinking price spread. In Europe, hike in ethylene oxide April contracts may impact MEG market, where margins are under pressure. In US, March MEG contracts rolled over on changing supply and demand fundamentals.

Polyester fibre chip market sentiment was stalemated in Asia while offers generally rolled over amid flat liquidity. Semi dull chip makers made sporadic cut in offers inventory creeped up amid moderate sales-production ratio. In Europe, bids and offers for PET were heard below March domestic levels, as demand remained sluggish and upstream weaker.

Feedstock ethylene prices plunged in Asia to a nine-week low, pressured by ample regional April shipments and bearish downstream markets in China. In Europe, April ethylene contract price was hiked 3% amid higher naphtha cost while spot market, although spot prices jumped as players prepared for spring maintenance starting April. In US, spot prices fell amid ample supply and lower upstream ethane costs

Paraxylene spot prices managed to float above the previous week’s levels in Asia as supply is expected to increase with the startup of a 2.25 million ton year plant in China. Contract price for April also failed to settle due to uncertain market. European market was soft following movements in Asian market while demand was termed as quiet, with ample availability. In US, spot declined on anticipated startups in China which is expected to expand global supply and decrease demand for US exports. Meanwhile, March paraxylene contract settled up from February.