Polyester price sobers as raw materials beat a hasty retreat

Polyester market momentum which had slowed down in the first week of September took to reversal in the second week of the month, just ahead of the peak season.

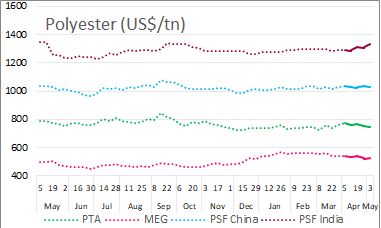

In China, polyester fibre (PSF) prices moved down as upstream cost retreated from a multi-year high. Nevertheless, polyester margins have also narrowed, while sales have slowed, resulting in reduction in operating rates of polyester facilities in key China markets. In contrast, PSF offers were hiked in Pakistan for the third week in a row, citing higher PTA and MEG prices on the international market in recent past. In India, producers’ prices were flat given the flatness in demand.

Polyester spun yarn prices also moved down in China in line with the fall in PSF prices, but the fall was not in same proportion and hence yarn makers enjoyed larger margins. In Pakistan, polyester yarn prices rolled over despite surge in PSF prices in past three weeks. In India, prices did not move as PSF prices went stable and recovery in currency pegged yarn values stable

Polyester filament (PFY) prices declined sharply on weak feedstock sentiment in China as downstream mills stayed by sideline or bought from hand to mouth volume expecting prices to lower given the fall in PTA and MEG cost. In Pakistan, selling indications for DTY were heard stable in Karachi market.

Raw materials beat a hasty retreat during the second week of September. Purified terephthalic acid (PTA) spot prices moderated in Asia while Futures in China saw steep decline as markets sentiment turned bearish following recent slowdown in polyester markets. European PTA market remained bullish amid tight supply and spike in paraxylene prices led to talk of significant price jumps in conversion fee. In US, PTA makers were preparing for Hurricane Florence as operation were likely to be affected. PTA supply in North America was extremely tight while strong paraxylene prices continued to drive PTA pricing.

Mono ethylene glycol (MEG) prices slumped nearly 7% in Asia as downstream polyester sales slowed down amid the US-China trade spat. Buying appetite were tapered as H1 September obligations were largely completed. In Europe, spot truck prices narrowed amid slightly muted activity while demand from antifreeze sector was healthy. In US, MEG supply and demand fundamentals were balanced and spot prices were holding steady from August.