Nylon chain pricing may fall as benzene slumps late October

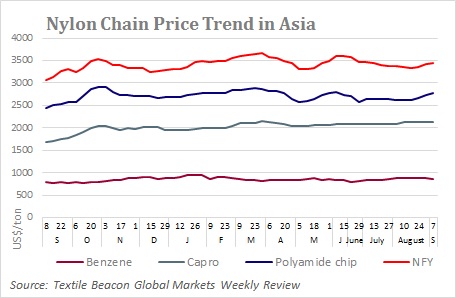

Nylon chain will soon be adversely impacted by falling benzene prices across regions. The impact will percolate through weakening caprolactum and nylon chip markets. Nylon chain pricing has largely driven by cost of late. Nylon, also known as polyamide, is used mainly in fibre and engineering polymer applications. Nylon fibre is used in apparel, carpets and home furnishings while nylon engineering resin is used in automotive parts.

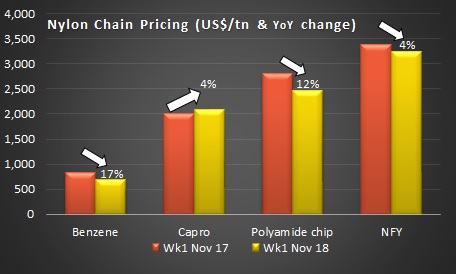

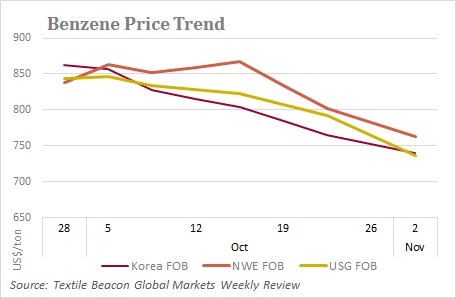

Benzene prices slumped in Asian markets on the back of the sharp pullback in crude futures and weak performance in downstream styrene market. A draw down in shore tank inventories along eastern China also failed to revive the market. Japan’s Nippon Oil settled its November Asia contract price at US$785 a ton CFR Asia, US$75 lower than October settlement. In Europe, benzene spot declined to a 23-month low while November contract settled at a decrease from October. November contract dropped Euro 24 to settle at Euro693 a ton CIF NWE (US$788 a ton, down US$51). In US, spot prices declined on falling crude oil prices and slower demand while November contract settled lower, marking the lowest number since October 2017. US November contract settled US cents 5 lower at US cents 280 per gallon FOB US Gulf.

Caprolactum markets in Asia were quiet amid uncertainty and volatile prices in domestic China. Major producers released their November offers slightly higher than October settlements. Sinopec nominated November contract price at 17,500 a ton (US$2,520 a ton, up US$20 from October settlement). In Europe, October contract discussions were concluded with drops due to lower October benzene costs. Meanwhile, precursor, cyclohexane November contract softened double-digits, marking the fourth consecutive monthly decreases

Nylon high-speed spinning chip offers fell on the back of weak caprolactum and weakening demand in the region. In China, prices of bright conventional chip picked up mainly for fishing net yarn or staple fibre production as distributors and converters were more positive on buying interest. In Europe, October discussions for nylon 6 and nylon 6,6 were concluded between rollovers to slight decreases. Contracts for nylon 6 virgin polymer material were at a Euro cent 0.01 decrease at the high end while nylon 6,6 virgin polymer material rose Euro cent 0.10 at the low end.

Nylon filament yarn (NFY) prices were mostly stable in China excepting some lower end prices edging down for few specs. The support mainly came from hike in domestic CPL spot and contact prices. Overall demand was passable and production was at break-even levels. In India, NFY prices remained unchanged as cost was still firm at high level.

(Source: Global Markets Weekly Review. For full report write to us at sales@textilebeacon.com)