Nylon prices to retreat slightly in December

After a marathonic run in the past 4-6 months, nylon chain pricing may see a reversal in December, although slightly, particularly in Asian markets. Nylon is still an industry with excessive supply, so prices have mostly depended on feedstock cost, while demand/supply fundamentals took a back seat.

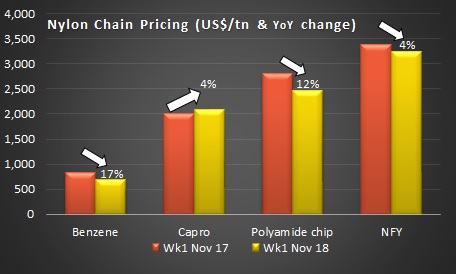

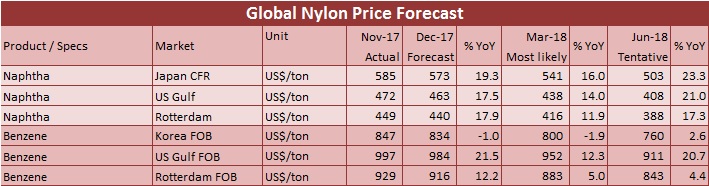

Going into December, benzene markets across region will tend to respond to the volatility in crude oil prices while narrow arbitrage between China and US would keep the Asian market under pressure. The probability of benzene values receding is much more evident although the first December Asian Contract price by Japan’s JXTG Nippon Oil & Energy settled at US$885 a ton, up US$80 from its November settlement. Spot has been behaving either sides and on many occasions were at a discount to contract numbers.

In Europe, an initial benzene contract for December settled at Euro 847 a ton, up Euro 145 from the previous month on robust demand. In US, too December contracts settled at US cents 330-340 a gallon FOB, US cents 46-53 higher from November. However, spot suggest that elevated prices are likely to dissipate over the month as refinery operating rates have improved and more import cargoes are fixed for shipment to the US in the coming weeks.

Asian caprolactum markets were steady to slightly weak in November looking at upstream benzene cost, and downstream markets. Markets in November was opposite to that of October; when spot prices decreased gradually every week. Going into December, most buyers will finish credit near year-end on concerns of rising inventory. Thus, cautious buying sentiment will prevail, and spot prices may tend to moderate as demand will weaken and buyers will lead the deals.

Nylon or polyamide chip markets were under corrections in the last two weeks of November in Asia as producers increased supply and downstream demand although changed for the better. Buyers were cautious towards high-priced goods and thus, nylon chip markets are expected to make no significant fluctuations in December and spot prices are likely to fall after six continuous months of increases.

Players in nylon filament yarn markets in Asia were less bearish about outlook as nylon chip markets are expected to turn for the better. However, given favorable margins in nylon yarn market, some producers may keep lowering prices to boost sales. However, supply/demand fundamentals will be normal as plants will operate stably, and buyers will cover short positions at low prices, leaving inventories at more than half a month’s worth. However, nylon is still an industry with excessive supply, so prices will also depend mainly on feedstock cost.

Source: Textile Beacon’s “Global Nylon Price Forecast” report of December 2017