Will Indian cotton emerge a winner in US-China trade war?

Indian cotton emerging as a winner amid ongoing trade war between US and China raises doubt given the prevailing market conditions and changing circumstances. The US on 15 June announced imposition of 25% tariffs on US$50bn worth of Chinese goods. The first wave – covering 818 products with a value of US$34bn – will take effect on 6 July, while tariffs on another US$16bn of Chinese goods to be applied later after soliciting public comment.

China retaliated by proposing to impose the same tariff rate against US goods worth US$50bn, to which the US responded with a threat of further tariffs on US$200bn of Chinese goods that will include a wide swath of oil and petrochemical products. Such reactive and punitive moves will only hurt both economies, with China being harder hit as it is an export-oriented economy. It will take long time to find substitute markets to replace the US, which accounted for about a 20% of China’s overall exports in 2017.

Impact on Global Price

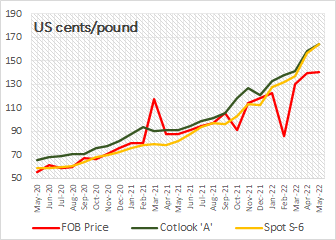

However, the impact on cotton market has been adversely following the spate between the two economies. Cotton global benchmarks are seeing free fall as the deadline of tariff imposition come closer. For cotton, US is the world’s biggest cotton exporter, while China is the top consumer.

The third week of June marked its worst week in nine months for cotton futures amid escalating trade tensions. The third month contract fell about 5% on the week, the biggest weekly decline since mid-September. Speculators were seen cutting their net long position in cotton while total futures market volume and open interest declined sharply.

As the month closed, June was marked as the worst monthly performance in nearly two years amid trade despite a bullish acreage report of the USDA. Speculators continued cutting their net long position in cotton in the last week of the month.

Between mid-June and end-June, the December contract has lost about 6% and near month July by more than 5%. Basically, cotton futures have risen as much as 21% this year mainly on drought eroding crop in West Texas, which shortened the crop amid stable demand.

The Cotlook ‘A’ Index representing global spot markets, had climbed above US cents 100 per pound in the first two weeks of June but dropped 8% to US cent US cents 93.25 per pound by month end.

Such drops in cotton price may continue as the trade war escalates going into the new marketing season. And if such eventuality happens, the price gap between Indian cotton and global markets will narrow down dramatically, prompting cotton buyers to scout for more cheaper and high-quality cotton elsewhere.

Benefits to Indian Cotton

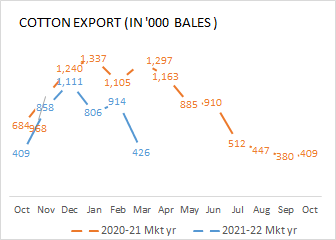

China has approved 800,000 ton (or 48 lakh Indian cotton bales) of additional cotton import quota for 2018, which confirmed the widely anticipated move by China to allow more overseas purchases. China has reportedly signed contracts for 5 lakh bales of cotton from India for the new cotton season. The additional quota procurement may start from 1 July. India is expected to benefit by at least selling 10-15% of that quantity. According to reports, China is likely to import at least 20 lakh bales from India in the season starting from October.

Indian exporters generally start selling new season cotton from August end after estimating the crop output, but robust demand from China and higher prices have prompted them to sign deals in advance. The weak INR makes India’s exports more appealing, and freight costs to the neighboring Asian country can be relatively cheap.

The pertinent question arise is that will the Indian cotton crop support this adventure. Crop sowing and weather report poses a gloomy picture as of now. Pan India, cotton is planted in about 32.2 lakh hectares as of 29 June, as against 46.10 lakh hectares in the same period last year. Sowing in Haryana has increased a bit, but has fallen in Punjab and Rajasthan. Maharashtra may witness some rise in the cotton acreage as farmers prefer cotton. In Gujarat, the pace of cotton sowing has been sluggish at 2.41 lakh hectares as of 25 June, down 64% from last year’s 6.76 lakh hectares at the same point of time. The rainfall has also been in deficit till June 30, pegged at 91% of State’s average.

Although the is a very early stage to gauge the crop, but things appear bleak as of now. In case, the crop is bumper, prices tend to move down concerns of surplus crop. This may weaken sentiment and cotton prices will come under pressure. However, the cushioning factor is the MSP on cotton which will be fixed at least 1.5 times of the production cost and may turn up to be higher than spot values in the new marketing year.

Can happen?

So, the euphoria of larger export and that too at better price can be short lived, as the crop size will depend on the temporal and spatial distribution of South West monsoon. Even more displeasing is that the crop size remains illusionary. The last year’s crop estimates are still not final, so ensuing crop is still far away.

Nevertheless, there are chances that China will still get cotton from the US, possibly indirectly. Mills may obtain some cargoes via Vietnam or buy American cotton directly by paying the high tariff.