Should India stop exporting cotton and ship more yarn?

The question becomes pertinent on two facts. First, the huge difference between price at which India export cotton and the price at which it ships out yarn. Second, most large textile economies like China and Bangladesh have climbed or moved up the textile value chain, from basic raw material like fibre to yarn further to fabric and to apparels and garment. Some economies not having indigenous basic raw material and depend on their imports, have started at upper value added level, like Bangladesh. It began with producing garments, integrated back to fabric and later to yarn spinning.

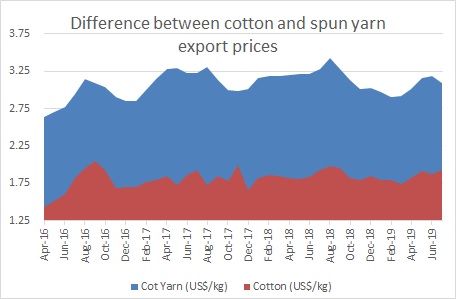

Over the past three years. India exported cotton at an average prices of US$1.80 per kg. During the same period, cotton yarn prices averaged US$3.07 a kg, all counts. This explains the huge difference between basic raw material and value added products. Yarn can earn atleast 50% more than the value of cotton that is exported. And that too, a large volume of fibre is exported Bangladesh, Vietnam and Pakistan, who in turn exports yarn and fabric back to India.

The same numbers for Bangladesh averages US$1.85 per kg for cotton and US$3.26 a kg for cotton yarn, implying that yarn fetches 75% more than simple cotton.

Two major textile association, CITI and Texprocil, have observed that the textile industry was underperforming, citeris paribus, due to sluggish exports, poor domestic demand, and growing imports from Bangladesh, China and Sri Lanka.

The Impact & benefits

- Stopping the white fibre export will shrink global supplies and prices will tend to rise. This will also be reflected in cotton yarn prices sooner or later.

- Producing and exporting value added products like yarn will attract investments and generate employment in domestic market

- More foreign exchange earnings (at least 50% more if yarn replaces cotton shipment) will provide stability of INR

- Instill competition among farmers to produce quality fibre and thereby increase their remuneration

What should change

Given the structure of Indian textile industry, most companies are family owned, and thereby limiting risk taking ability. The domestic market being so huge, exporting yarn has been taking a back seat. Quality and delivery will have to be pushed closer to international standards to maintain continuous business.