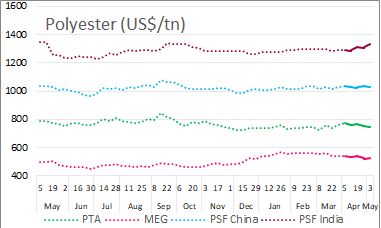

Polyester inputs mixed in second week of February

Polyester inputs or intermediates markets were mixed in the week ended 15 February, with purified terephthalic acid (PTA) prices rising in China and edging down outside China in Asia while contracts were up in Europe . Paraxylene markets inches up in Asia while Europe follow-up.

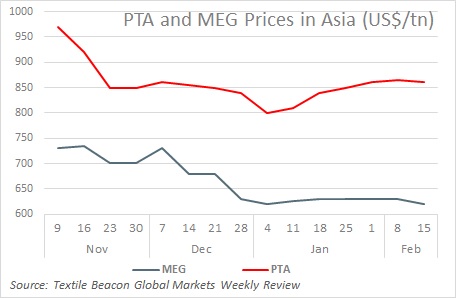

Purified terephthalic acid

PTA price movement was mixed during the week with benchmark China spot rising while Korea/Taiwan markers edging down. In China, futures market also dropped in smaller range owing to the news about plant maintenance. From the fundamental point of view, there is no unfavorable factor for the market, but lacks momentum to go up in a short term. Thus, the market is expected to resist price drop and may fluctuate widely on the whole. In Europe, contract for February were hiked moving alongside February paraxylene. Downstream PET market attributed the upward pressure to rising spot prices in Asia. PTA is a key polyester inputs.

Paraxylene

Paraxylene prices in Asian markets inched up this week but are expected to remain supported by healthy market fundamentals going forward, as supply pool is seen decreasing as a many units will undergo maintenance works. The current market structure is in a contango, reflecting more than sufficient supply for prompt materials. Supply for prompt materials was ample as a reduction of operating rates at downstream PTA units in China seen during Q4 2018, resulting in less demand, and a buildup of PX inventories. In Europe, spot supply was balanced with good demand, prompting prices to inch up a bit. Meanwhile, February contract price was settled at an increase attributed to downstream PET market and rising Asian spot prices. In US, paraxylene spot prices remained flat as upstream mixed xylenes are likely to maintain premium over other aromatics for the rest of Q1 amid tight supply and stronger margins for derivative paraxylene.

Mono ethylene glycol

MEG prices trended lower in Asian markets this week as downstream polyester sales remained slow after Chinese New Year. There was also a downward pressure on prompt arrival cargoes and domestic cargoes in China due to downstream buying had not begun after the holiday. Downstream were still recovering and may only resume normal operations around end February. Meanwhile, concerns over a slowdown in Chinese economy also dampened sentiment. Inventories along east China increased 27% to 1.14 million tons. Meanwhile, MEGlobal nominated its March Asian Contract Price higher from February. No report or update was available from European US markets this week hence prices are notionally rolled over. MEG, another key polyester inputs accounts for 0.35 unit in 1 unit of PSF.

Source: Global Markets Weekly Review