PTA makers enjoying healthy margins, but will they continue?

PTA (purified terephthalic acid) producers across Asia, Europe and US have been mostly enjoying healthy margins, on the back of steady growth in demand from polyester markets while firmer upstream energy complex and paraxylene prices have buoyed prices in recent weeks.

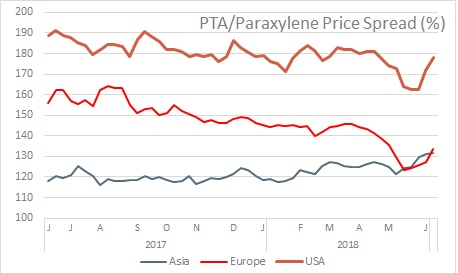

The spread between PTA (end product) and paraxylene (input), the basic barometer of a healthy relationship, has been strong across regions but were seen weakening in Europe since November last. Nevertheless, the spread picked up dramatically in early May in Asia and Europe, and later in US. But this expansion was mainly due to polyester bottle grade chips markets rather than textiles.

In Asia, the spread between PTA FOB Korea and paraxylene CFR Southeast Asia was at its yearly peak of 130% or US$204 per ton in first half of June, buoyed by rising PTA prices and flat paraxylene cost. The rise emerged due to supply shortage amid modestly growing demand. Within Asia, the Southeast saw plant outages and had to buy cargoes from Northeast which pulled up prices across the region in the past two months.

The H1 2018 saw strong growth in demand in the downstream polyester markets in Asia, particularly China, which supported the rally in PTA prices amid tight supply. Asia’s prices are currently stable at high levels, with regional buyers preferring need-to basis cargoes.

Going into H2 2018, PTA supply in Asia is expected to lengthen as new capacities start-up in India and China. These supplies will come when demand will slowdown, especially from textile segment while bottle chip market has some more appetite.

Major plants will also resume production after unplanned outages to ease the current global supply tightness that has been driving up Asian prices, while demand typically weakens in the third quarter. Thus, prices in Asia may come under pressure as fresh supply will hit the markets when new major regional plants start production in the third quarter.

JBF Group’s 1.25 million ton a year PTA unit in Mangalore, India is slated to to start up in Q3, although the schedule is still uncertain. In China, Fuhaichuang Petrochemical, is planning to resume operations at its complex in Q3 after a prolonged shutdown. Its complex in Zhangzhou has a 4.5 million ton a year PTA plant, which is comprises three lines, two of which are in operation since end-2017. The third line is likely to restart once the operations at its upstream paraxylene unit at the site smoothens.

Reports indicate that market sentiment is pessimistic about the outlook. But this can change if there is sudden uptick in downstream demand.

In Europe, Indorama Ventures Portugal plans to start up in July its idled 700 kilo ton a year PTA unit in Sines. Thailand-based Indorama Ventures acquired the plant from Portuguese Artlant PTA in late 2017.

All these factors may lead to narrowing of the price spread between PTA and paraxylene as paraxylene rely on downstream for strength. Future movement will also depend on market conditions in the downstream polyester industry, especially in the downstream polyethylene terephthalate markets in the short run.

In Europe, BP Chemical on 15 April declared a force majeure at its Belgium PTA unit, and declared a second force majeure on 17 May; while PKN Orlen on 23 April declared a force majeure at its Wloclawek PTA unit in Poland which was subsequently lifted on 2 May, with spot cargoes from the plant limited until after a planned maintenance in September/October 2018.

PTA June contract in Europe were increased by Euro40 a ton to Euro723-757 a ton FD NWE. The settlement moved alongside June prices in paraxylene contract. PTA supply remained tight due to a continued force majeure at BP in Belgium and a recent force majeure declaration at Hanwha General Chemicals in South Korea. Production problems have caused chaos in PET market, but production was slowly improving as PTA allocation from BP gradually increased.

This has help significant improvement in the spread between PTA and paraxylene to 130% in June. However, it is much lesser than the 160% a year ago.

In US, too the spread was closing towards 180% after PTA contract for May was raised while spot paraxylene was tumbled on expectations of improved supply and weaker downstream demand. The market expects an imminent restart of a BP paraxylene production unit that has been down since early April. Downstream demand weakened amid BP’s limited sales allocation, reports said.